Looking Down the Money Trail at CSPA

I attended CSPA’s “Looking Down the Money Trail” tonight at Pillsbury in Palo Alto. Pillsbury hosts a number of entrepreneur oriented events and tonight their room was overflowing. One reason was that the event had a stellar panel:

- Steve Bengston, Managing Director of Emerging Company Services (ECS), PricewaterhouseCoopers

- Prashant Shah, Managing Director, Hummer Winblad Venture Partners

- Ashmeet Sidana, General Partner, Foundation Capital

- John Steuart, Managing Director, Claremont Creek Ventures

- Gus Tai, General Partner, Trinity Ventures

Steve Bengston led off with are recap of the Q3/2008 PWC Moneytree results, so this was a retrospective in terms of the data that was presented. The top six most active firms (by deal count) in Q3 were Draper Fisher Jurvetson 26, Intel Capital 20, New Enterprise Associates 19, Kleiner Perkins 18, Sequoia 17, and U.S. Venture Partners 17. Silicon Valley investments totaled 2.77 billion dollars in Q3, down about 3% from Q3/07’s 2.88 billion and about 10% from Q2/08’s 3.11 billion. Silicon Valley accounted for about 40% of the total US VC investment across all three time periods.

Key comments from the panel caught my attention (all are paraphrased from my notes):

- John Steuart: healthcare consumes a significant and growing fraction of US GDP, we Claremont believe that enormous opportunities exist to build multiple large firms bringing Moore’s Law to medicine.

- Ashmeet Sudra, in response to a question about the role of government helping innovation and entrepreneurship: California’s ban on non-competes (except in the case of the sale of a business) has done more to take the shackles off of entrepreneurs than any other government action.

- Prashant Shah, in response to role of government question: government can make the long term investment in basic research that VC’s cannot. Basic research is the foundation for new technology entrepreneurship.

- Gus Tai (very paraphrased): I am interested in software & SaaS offerings that can be distributed at no charge or low cost to individuals but once it reaches a critical mass of five users in the enterprise can be priced at value. He cited Zone Labs as an example: they offered a free personal firewall that enterprises had to pay for, when they discovered five at the same IP address they contacted them and asked them to convert from free to paid.

Some consensus answers (echoed by more than one panel member).

- No B rounds right now (either they are re-priced / down rounds as a second A or there is clearly enough traction so that it can be priced as a C round).

- The credit crisis has caused some Limited Partners to pull back or withdraw from some commitments, making it much harder to close new funds and forcing some existing funds to re-open or add annexes.

- What’s hot? Anything with a “hard ROI” (clear cost savings attached) or attacking an existing cost stream that has paying customers.

- K12 education is another area that government plays a critical role in laying the foundation for innovation and entrepreneurship.

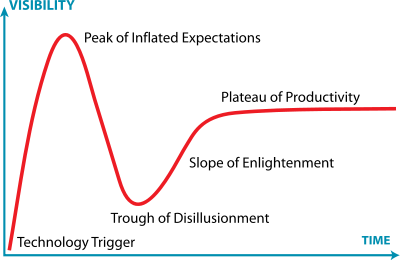

- The first 25-50 million in revenue can proceed from a very narrow observation of what can drive revenue in a niche. Domain expertise and intimacy with a problem make all of the difference early on, later you need experience building a large company. There are two points in the Gartner hype cycle when that narrow observation has the most value (because of the highest risk of being wrong) before the technology trigger brings the market into existence and in the “trough of disillusionment when no one is sure when the real market will materialize.

Related Blog Posts

- Recap From “Startups: What’s Hot, What’s Not (2018)” Today at WIC

- Startups: What’s Hot, What’s Not Feb-22-2022

- Startup Funding August 2023: What’s Hot and What’s Not!

Note: Gartner Hype Cycle image by Jeremy Kemp, used under Creative Commons Attribution Share Alike License

“K12 education is another area that government plays a critical role in …”

I don’t understand this. Is the panel suggesting that there might be a surge in entrepreneurial activity in the education sector in 2009? Or that there won’t be unless the government helps out?

I think the context was that government investment in K12 education could have a significant impact on entrepreneurial activity by better preparing folks for life. It was part of a discussion that involved investment in basic research vs. direct investment in startups and the consensus was that government would be better investing in key enablers to entrepreneurial activity instead of directly in startups.