Q: How Do I Value an Equity Offer From a Startup?

Some suggestions for how to value an equity offer from a startup as part of a decision on whether to join.

Q: How Do I Value an Equity Offer From a Startup? Read More »

Some suggestions for how to value an equity offer from a startup as part of a decision on whether to join.

Q: How Do I Value an Equity Offer From a Startup? Read More »

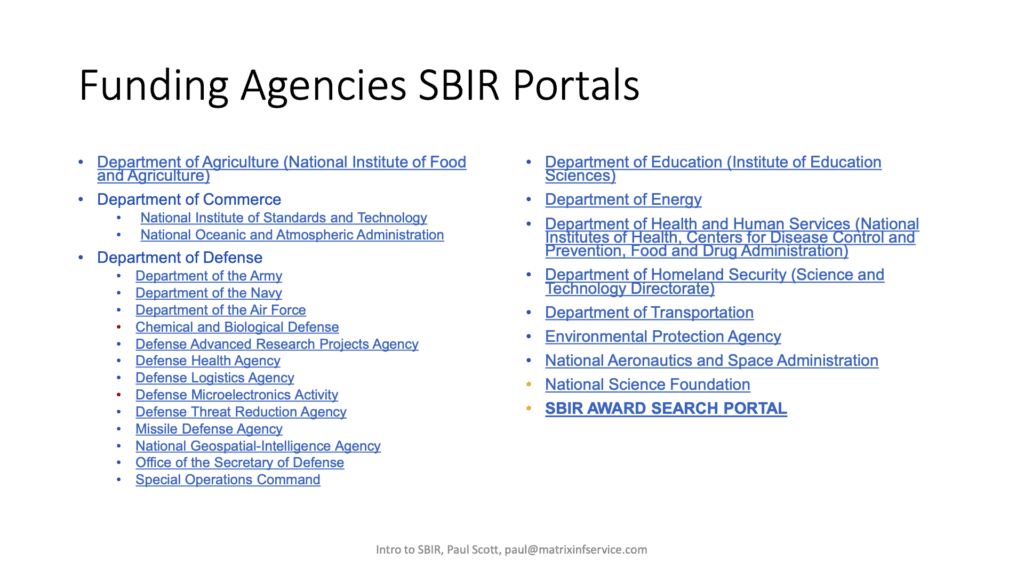

Paul Scott’s expert guidance on the SBIR grant process, from concept paper to full proposal.

Paul Scott’s expert guidance on the SBIR grant process Read More »

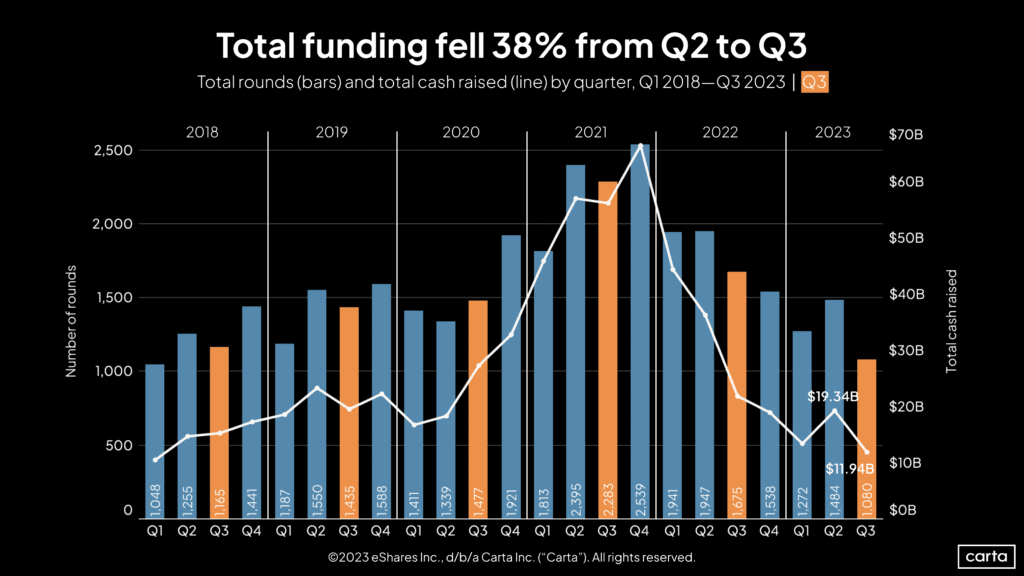

State of the Tech Markets in Jan-2024: a discussion among David Weisburd, Bill Gurley, Brad Gerstner, and Jason Calacanis shed light on the challenges faced by startups, drawing parallels to the dotcom crash. Gurley, Gerstner, and Calacanis on the State of the Tech Markets in Jan-2024 In a Jan-6-2024 conversation (on Episode 1875 of

Gurley, Gerstner, and Calacanis on the State of the Tech Markets in Jan-2024 Read More »

Startup Funding 2023 – On August 10, 2023, Procopio hosted a panel of VCs to share the state of startup funding.

Startup Funding August 2023: What’s Hot and What’s Not! Read More »

Many digital nomads and travelers to Silicon Valley are looking for good networking events to meet and compare notes with other founders. This guide gives an overview of networking and startup events in Silicon Valley.

Guide to Silicon Valley Startup Events Read More »

Before paying money to pitch, it’s important to ask relevant questions to ensure you make an informed decision. Pitching to investors may secure funding and help accelerate your business. Here are questions you should consider asking before you sign up for a pitch competition: What is the format and duration of the pitch event? Understanding

8 Questions to ask before signing up for a pitch competition Read More »

A Minsky boom is a period of economic growth characterized by increasing instability and speculation, ending in startup funding constricting.

Clear in Hindsight: April 2022 ended a Minsky boom for startups Read More »

Paul Scott of Matrix Information Services gives a briefing on SBIR Grants and how they can be used to secure funding without dilution.

Funding Without Dilution: Introduction to SBIR Grants Read More »

An extract from a highly interactive session with Thomas Ahn at the Lean Culture Meetup on Mar-25-2021 where he answers “what makes for an effective investor pitch?”

Micro-VC / Angel investor Thomas Ahn on the Effective Investor Pitch Read More »

Lean Canvas Finances is part of a five part series by Ed Ipser where he explains how to use the Lean Canvas and what it is good for. Focus Marketing Operation Finances Experimentation In this Lean Canvas – Finance session, Ed Ipser shares how to identify your own revenue and cost structure and how to create

Lean Canvas Finances Read More »

Paul Scott shares lesson learned writing SBIR grants. His presentation covers the Grant Writing Application Process.

Lean Culture: Seed Funding Without Loans – An Introduction to SBIR Grants Read More »

This post explores meaning of financial capital for bootstrappers. It addresses the real costs of market exploration and product validation and verification.

A Practical Introduction to Financial Capital for Bootstrappers Read More »

A summary of my talk at Women in Consulting lunch meeting today on “Startups: What’s Hot / What’s Not (2018).” Includes slides and links to sources.

Recap From “Startups: What’s Hot, What’s Not (2018)” Today at WIC Read More »

If you have bootstrapped your startup to the point where you have a business that both merits and would benefit from outside investment then you may need to consider seeking investment. Here are some common formats we have seen for an investor presentation.

Investment Presentation Formats Read More »

If you want to be a succeed as a bootstrapper, start with what you’ve got: you have an insight into an opportunity, a marketing edge, a particular problem where you’re going to bring distinctive value.

Successful Bootstrappers Are Trustworthy Salespeople Committed to Customer Satisfaction Read More »

Dan Scheinman (@dscheinm) graduated from Duke Law School in 1988 and went to work as an associate at DLA Piper before joining the Cisco legal department. Once inside he worked his way up to General Counsel, then ran corporate development which included managing minority investments and acquisitions, and finally was general manager for Cisco’s Media Solutions

Dan Scheinman’s Blue Ocean Venture Strategy: Target Entrepreneurs Over 35 Read More »

Here are some back of the envelope models to estimate prospect counts and market size.

Q: How To Estimate Prospect Counts and Market Size Read More »

Tim Draper, founder of VC firm Draper Fisher Jurvetson, is taking a holistic approach to entrepreneurial education with Draper University in San Mateo.

Draper University of Heroes Takes Holistic Approach to Teaching Entrepreneurship Read More »

Ryan Waggoner wonders if the popularized approach to startups is wrong. Instead of putting health and relationships at risk, try patience and humility.

Ryan Waggoner: Maybe Startups Are So Hard Because We’re Doing Them Wrong Read More »

This “time capsule” post from 2012 lists some useful tools like MyPermissions, SocialMention, and HackerFollow that are now defunct.

Three Useful Tools: MyPermissions, SocialMention, HackerFollow Read More »